Regulation in Property Valuation & Wealth Management: Opportunities Instead of Obstacles

Dennis Ritter

A regulatory shift is imminent, because since the introduction of CRR III on 1 January 2025 as well as the ongoing requirements from MiFID II, the hurdles for banks, asset managers and real estate advisors are rising. However, behind the regulatory complexity there is also enormous potential for optimisation if you use the right digital tools.

Why regulation means not only risk, but also opportunity

The regulatory wave continues to roll. Capital requirements are rising, documentation obligations are increasing and ESG criteria are becoming the norm. Particularly affected: property valuations and wealth management.

CRR III brings new standards to property valuation with the term "Property Value". MiFID II, on the other hand, demands full transparency in the investment advisory process. Classic tools like Excel lists are no longer sufficient here.

New requirements for property valuation – what is changing

From market value to Property Value

The "Property Value" according to CRR III must be conservative, transparent and realisable in the long term. Expected price increases must not be factored in. Two procedures are available:

Mortgage lending value method according to BelWertV

Here, the property value is determined on the basis of the mortgage lending value. This is the value that can be achieved in the long term and was already regulatorily established in the past. This procedure corresponds to the German Mortgage Lending Value Determination Regulation (BelWertV) and is particularly suitable for banks that have to meet high documentation standards.

Market value method with portfolio adjustment

Alternatively, the current market value can also be used. However, only on the condition that a downstream review is carried out. This must ensure that the value is not above the long-term sustainable level. The adjustment can be made on a portfolio basis using statistical market data.

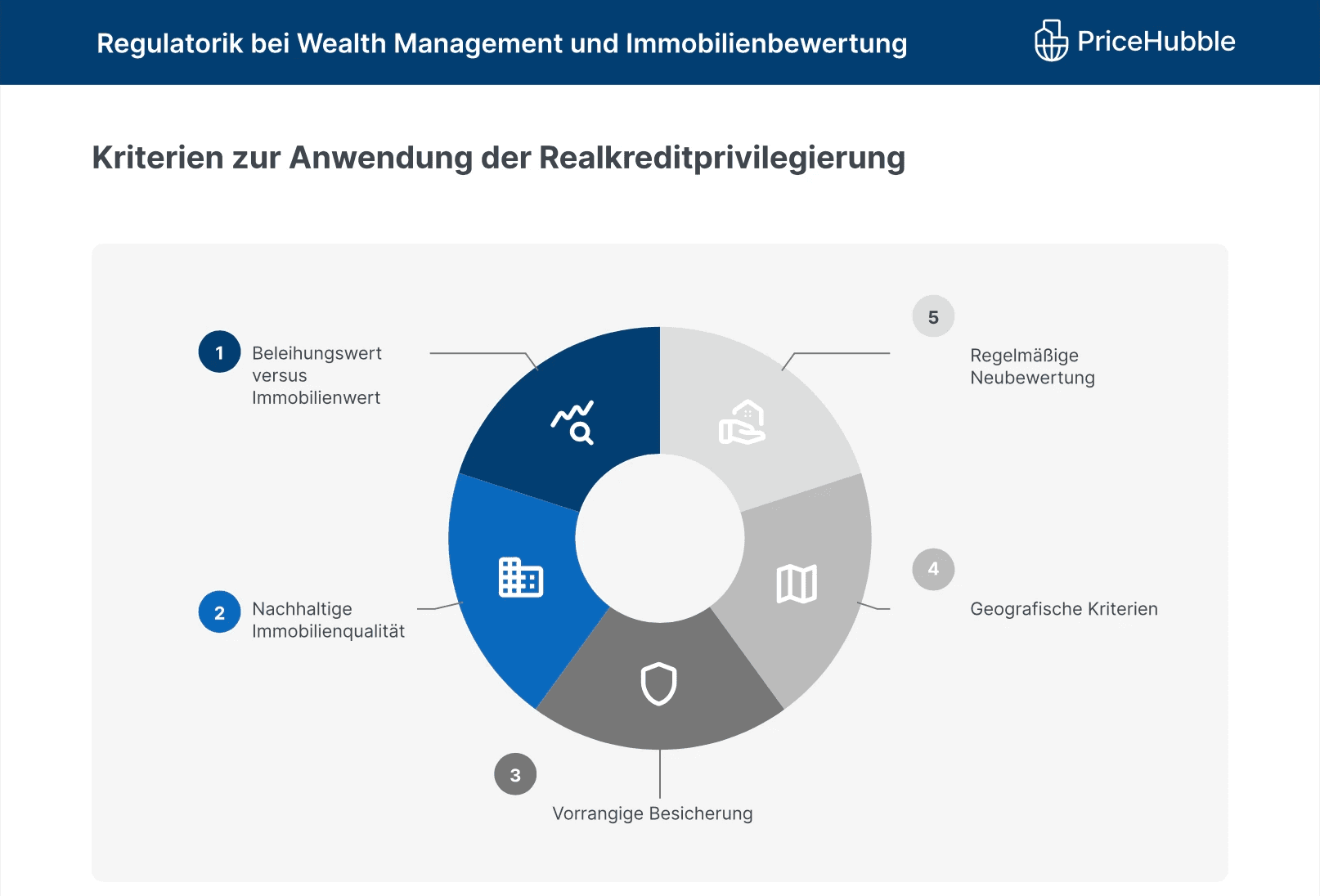

Real estate lending privilege and risk weights

Real estate-backed exposures are now categorised more strictly:

Residential real estate

Commercial real estate

ADC (Acquisition, Development, Construction)

This distinction has a massive impact on capital requirements. An incorrect classification approach can lead to a risk weight of up to 150%. More precise definitions of these terms can be found in the white paper 'Regulation in Digital Wealth Management and Property Valuation'.

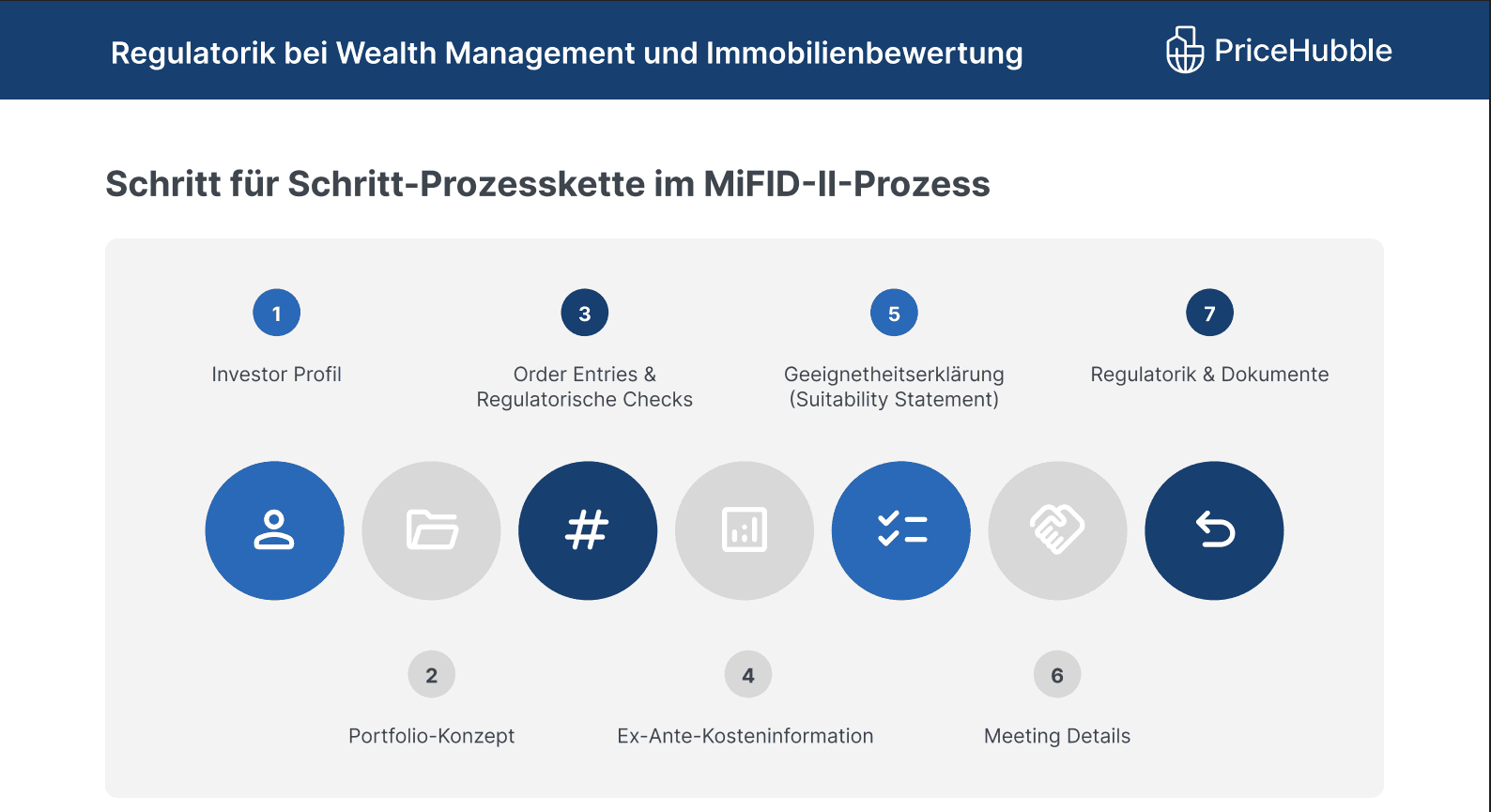

Wealth Management between efficiency and compliance

MiFID II forces banks into seamless suitability testing, product recommendation justification and cost transparency. This leads to longer consultation processes, which often take over 60 minutes.

The solution: automated, digital processes that seamlessly integrate regulation without compromising the quality of advice.

The digital answer: fincite • cios & PriceHubble

One system for everything

The software solution fincite • cios offers an All-in-One Wealth Management Software that covers the entire value chain from onboarding to reporting. Integrated features include:

MiFID II-compliant advisory process

Suitability reports & ex-ante cost information

Regulatory control mechanisms with automated documentation

Average time savings: 12 weeks per advisor per year.

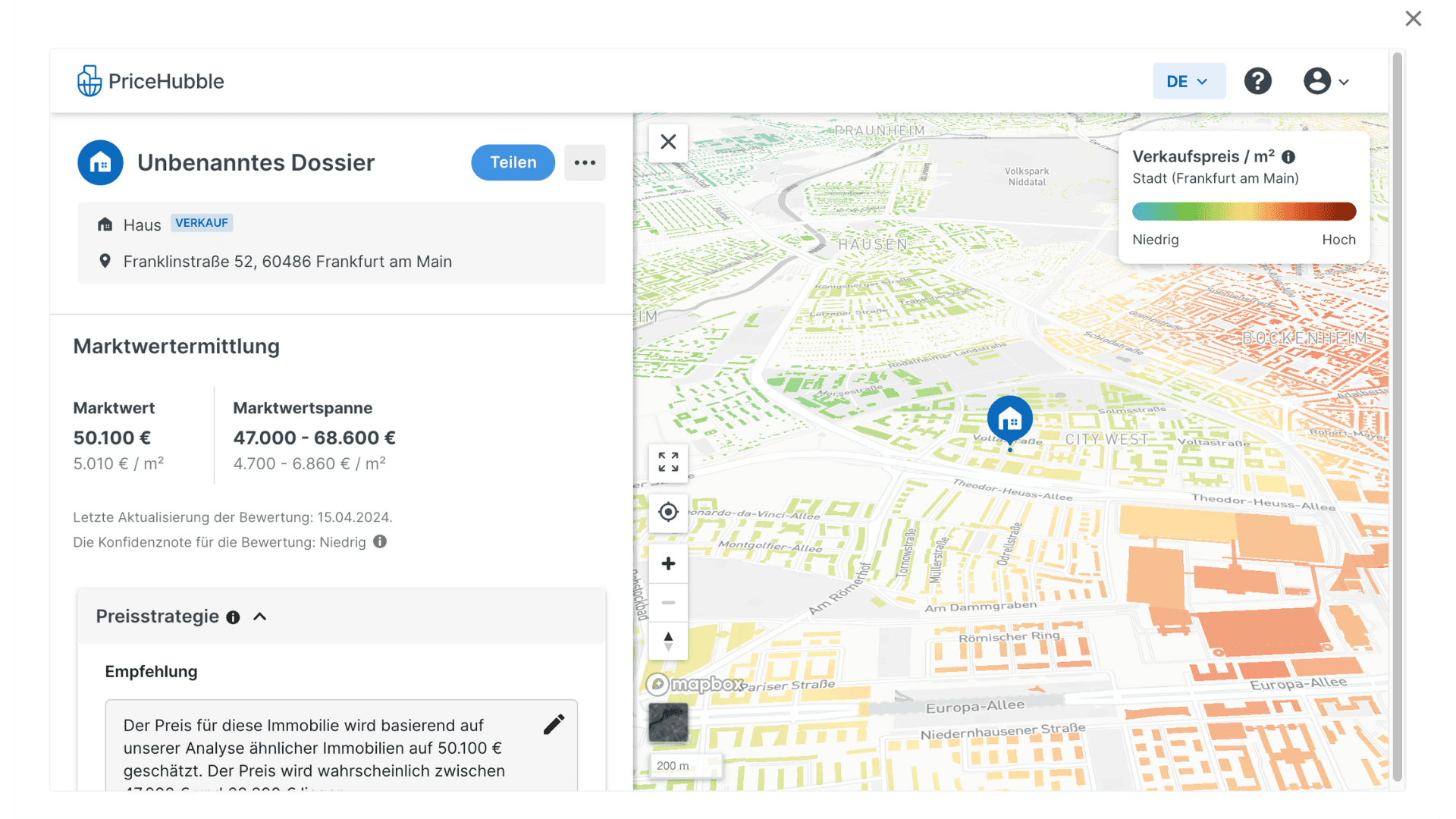

Property valuation meets AI

PriceHubble complements fincite • cios with a data-driven, EBA-compliant valuation of properties, including:

Live market analysis

Determination of the conservative "Property Value"

Integration into total assets and portfolio allocation

Automatic monitoring & recommendations for action

The 360° aggregation of all client assets, including real estate, represents another key advantage. Through the integration with PriceHubble, property values can be assessed in real-time and included in the total asset analysis. This allows for a more precise asset allocation and opens up new advisory approaches that take into account the entire wealth spectrum of the clientele.

- Dennis Ritter, Lead Private Banking Germany, fincite

Conclusion: Those who take digitalisation seriously win twice on the regulatory front

The combination of digital tools and regulatory expertise enables not only clean compliance with requirements, but also strategic advisory competence with real added value for clients.

Take the opportunity now to restructure your compliance management. Efficient, secure and future-oriented. Do you want to know how you can provide advice more efficiently from a regulatory standpoint or how you can implement the solution directly?

Then download the full white paper from fincite & PriceHubble now or contact our WealthTech experts and arrange a free consultation. We look forward to hearing from you!

Frequently Asked Questions

What is CRR III?

CRR III (Capital Requirements Regulation III) is a revised EU regulation applicable from January 2025 that defines new capital requirements for banks. Among other things, it includes stricter requirements for property valuation, such as the introduction of the term "Property Value", as well as new risk weights for residential and commercial real estate. The goal is a more stable capital adequacy and more realistic valuation of collateral.

What impact does CRR III have on property valuation?

CRR III obliges banks to value properties more conservatively. Expected price increases must not be taken into account. Instead, methods such as the mortgage lending value method or an adjusted market value method are used. This adjustment directly affects the capital requirements and the risk assessment of real estate loans.

How does MiFID II affect the investment advisory process?

MiFID II increases the requirements for transparency and documentation in the investment advisory process. Advisors must provide proof of a suitability test, full cost transparency and a product-related advisory history. Digital tools such as fincite • cios help to implement these regulatory specifications efficiently and in an audit-proof manner.

Why is digitalisation crucial for regulatory processes?

Without digital processes, compliance with current regulations such as CRR III or MiFID II is hardly possible in an efficient manner. Manual workflows are prone to errors and time-consuming. Platforms such as fincite • cios enable automated, legally compliant advice, including documentation, reporting and property valuation in real-time.

What advantages does the integration of property valuations offer in investment advice?

By integrating up-to-date property values, for example via PriceHubble, banks and advisors can realistically map the client's entire wealth. This improves asset allocation, opens up new cross-selling opportunities and strengthens client loyalty through comprehensive advice.