Product

Clients

About us

Knowledge Hub

Onboarding

Watch the Onboarding Tutorial

Product

Clients

About us

Knowledge Hub

Onboarding

Watch the Onboarding Tutorial

Product

Clients

About us

Knowledge Hub

Onboarding

Watch the Onboarding Tutorial

WealthTech Trends 2026:

Who leads, who follows

WealthTech Trends 2026:

Who leads, who follows

3 reasons to read the radar:

3 reasons

to read the radar:

In the WealthTech Radar 2026, 12 industry experts analysed 11 future topics. It is not a trend report, but a concrete blueprint for anyone who wants to lead in Europe's wealth management industry.

11 deciding trends

From AI and cloud sovereignty to tokenization and digital estate planning. The topics that will make a difference in 2026.

From AI and cloud sovereignty to tokenization and digital estate planning. The topics that will make a difference in 2026.

+70 pages analysis

No theory, but well-founded analysis with concrete recommendations for banks, asset managers, and advisors.

No theory, but well-founded analysis with concrete recommendations for banks, asset managers, and advisors.

12 expert opinions

Voices from banks, WealthTechs, and consulting firms including Harvest, DWS, Morningstar, Allianz, and Upvest.

Voices from banks, WealthTechs, and consulting firms including Harvest, DWS, Morningstar, Allianz, and Upvest.

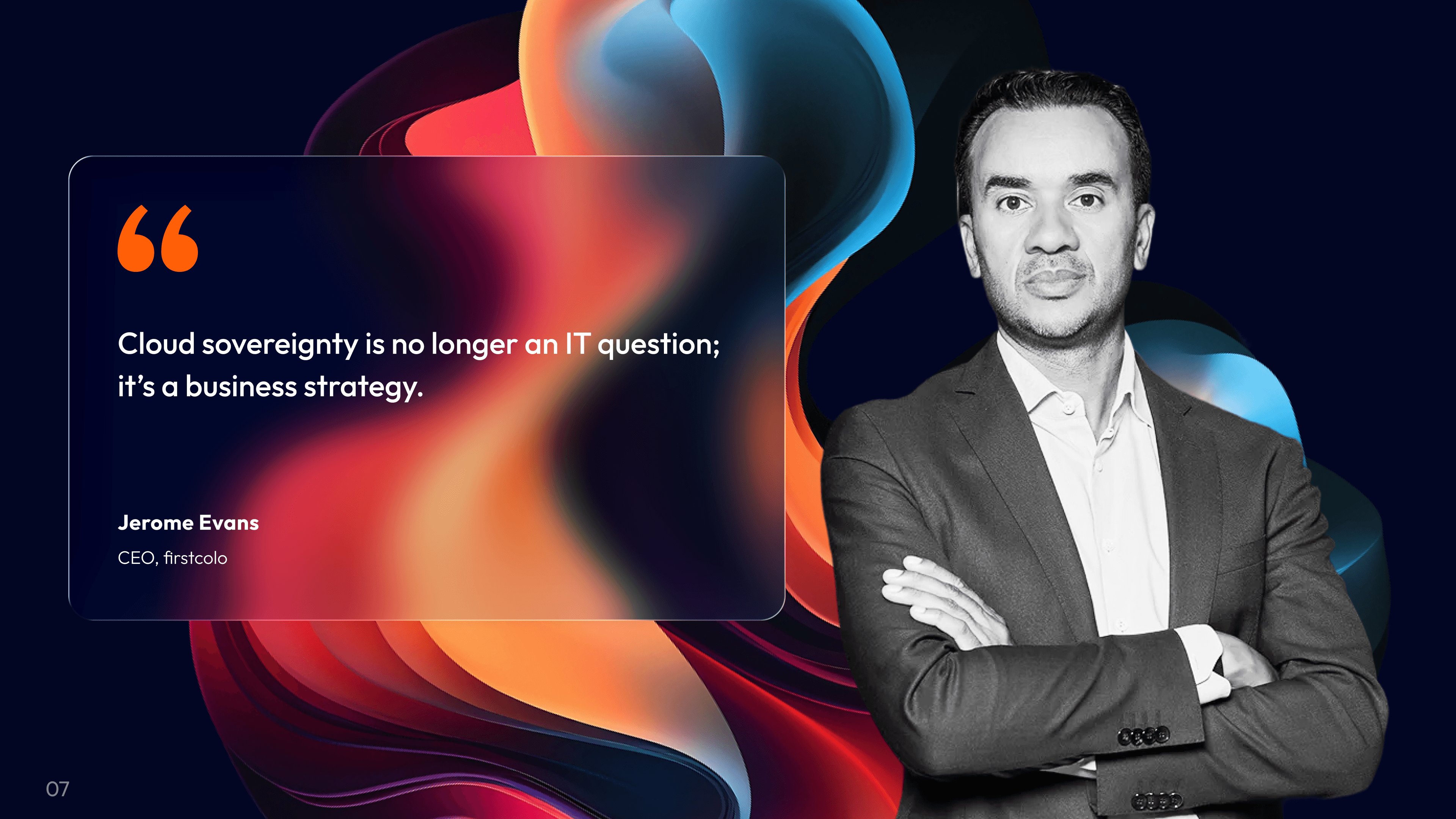

Cloud sovereignty is no longer just an IT issue, but a business strategy.

Jerome Evans

CEO, firstcolo

Tokenized Private Credit remains the fastest growing segment as a niche – bankable, provided governance, data, and infrastructure are in place.

Simon Seiter

Managing Director and CFO / CPO, AllUnity

Where traditional indices provide efficiency, Direct Indexing offers institutional control.

Alexander Sperlich

Managing Director for Germany / Austria / Switzerland, Head of Strategic Business Development EMEA, Morningstar

Data, precise assessability, and digital access make real estate a more attractive and strategically relevant investment component.

David Niedzielski

Managing Director, Sprengnetter Group

Digital securities infrastructure is no longer an experiment, but the foundation for the future of wealth management.

Dr. Til Rochow

CPO & Co-Founder, Upvest

The aggregation of wealth data combined with AI enables significantly more personalised financial products, recommendations, and advice.

Susanne Krehl

Chief Growth Officer, wealthAPI

Access is broadening, yet private equity remains a long-term investment heavily influenced by the respective manager.

Leyla Kunimoto

Founder, Accredited Investor Insights

Artificial intelligence does not replace humans; it enhances their decision-making capabilities.

Delphine Asseraf

Deputy CEO, Harvest

Anyone looking to tap into digital customer segments or offer more to existing customers should focus on establishing targeted offerings around crypto-assets.

Dr. Alexander Bechtel

Global Head of Digital Products, DWS

Digital assets are increasingly becoming a staple of the global financial markets.

Pablo Nobre dos Reis

Digital Products Analyst, DWS

Greenwashing was yesterday. Those who say ESG must now provide evidence.

Dr. Oliver Pfeil

Chairman of the Management Board of ÖKOWORLD AG

No digital idleness: Your assets require careful planning; otherwise, they will be lost.

Nicola Alvaro

Head of Wealth Services & Distribution, Allianz Life Luxembourg S.A.

Cloud sovereignty is no longer just an IT issue, but a business strategy.

Jerome Evans

CEO, firstcolo

Tokenized Private Credit remains the fastest growing segment as a niche – bankable, provided governance, data, and infrastructure are in place.

Simon Seiter

Managing Director and CFO / CPO, AllUnity

Where traditional indices provide efficiency, Direct Indexing offers institutional control.

Alexander Sperlich

Managing Director for Germany / Austria / Switzerland, Head of Strategic Business Development EMEA, Morningstar

Data, precise assessability, and digital access make real estate a more attractive and strategically relevant investment component.

David Niedzielski

Managing Director, Sprengnetter Group

Digital securities infrastructure is no longer an experiment, but the foundation for the future of wealth management.

Dr. Til Rochow

CPO & Co-Founder, Upvest

The aggregation of wealth data combined with AI enables significantly more personalised financial products, recommendations, and advice.

Susanne Krehl

Chief Growth Officer, wealthAPI

Access is broadening, yet private equity remains a long-term investment heavily influenced by the respective manager.

Leyla Kunimoto

Founder, Accredited Investor Insights

Artificial intelligence does not replace humans; it enhances their decision-making capabilities.

Delphine Asseraf

Deputy CEO, Harvest

Anyone looking to tap into digital customer segments or offer more to existing customers should focus on establishing targeted offerings around crypto-assets.

Dr. Alexander Bechtel

Global Head of Digital Products, DWS

Digital assets are increasingly becoming a staple of the global financial markets.

Pablo Nobre dos Reis

Digital Products Analyst, DWS

Greenwashing was yesterday. Those who say ESG must now provide evidence.

Dr. Oliver Pfeil

Chairman of the Management Board of ÖKOWORLD AG

No digital idleness: Your assets require careful planning; otherwise, they will be lost.

Nicola Alvaro

Head of Wealth Services & Distribution, Allianz Life Luxembourg S.A.

Cloud sovereignty is no longer just an IT issue, but a business strategy.

Jerome Evans

CEO, firstcolo

Tokenized Private Credit remains the fastest growing segment as a niche – bankable, provided governance, data, and infrastructure are in place.

Simon Seiter

Managing Director and CFO / CPO, AllUnity

Where traditional indices provide efficiency, Direct Indexing offers institutional control.

Alexander Sperlich

Managing Director for Germany / Austria / Switzerland, Head of Strategic Business Development EMEA, Morningstar

Data, precise assessability, and digital access make real estate a more attractive and strategically relevant investment component.

David Niedzielski

Managing Director, Sprengnetter Group

Digital securities infrastructure is no longer an experiment, but the foundation for the future of wealth management.

Dr. Til Rochow

CPO & Co-Founder, Upvest

The aggregation of wealth data combined with AI enables significantly more personalised financial products, recommendations, and advice.

Susanne Krehl

Chief Growth Officer, wealthAPI

Access is broadening, yet private equity remains a long-term investment heavily influenced by the respective manager.

Leyla Kunimoto

Founder, Accredited Investor Insights

Artificial intelligence does not replace humans; it enhances their decision-making capabilities.

Delphine Asseraf

Deputy CEO, Harvest

Anyone looking to tap into digital customer segments or offer more to existing customers should focus on establishing targeted offerings around crypto-assets.

Dr. Alexander Bechtel

Global Head of Digital Products, DWS

Digital assets are increasingly becoming a staple of the global financial markets.

Pablo Nobre dos Reis

Digital Products Analyst, DWS

Greenwashing was yesterday. Those who say ESG must now provide evidence.

Dr. Oliver Pfeil

Chairman of the Management Board of ÖKOWORLD AG

No digital idleness: Your assets require careful planning; otherwise, they will be lost.

Nicola Alvaro

Head of Wealth Services & Distribution, Allianz Life Luxembourg S.A.

12 high-profile experts as co-authors

12 high-profile experts as co-authors

12 experts as co-authors

12 experts as co-authors

Leyla Kunimoto

Founder

Accredited Investor Insights

Dr. Alexander Bechtel

Global Head of Digital Products

DWS

Delphine Asseraf

Deputy CEO

Harvest

Simon Seiter

Managing Director and CFO / CPO

AllUnity

Dr. Til Rochow

CPO & Co-Founder

Upvest

Dr. Oliver Pfeil

Chairman of the Board

ÖKOWORLD AG

Jerome Evans

CEO

firstcolo

Alexander Sperlich

Managing Director DE/ AT/ CH,

Morningstar

David Niedzielski

Managing Director

Sprengnetter Group

Susanne Krehl

Chief Growth Officer

wealthAPI

Pablo Nobre dos Reis

Digital Products Analyst

DWS

Nicola Alvaro

Head of Wealth Services & Distribution

Allianz Life Luxembourg Ltd.

Leyla Kunimoto

Founder

Accredited Investor InsightsDr. Alexander Bechtel

Global Head of Digital Products

DWSDelphine Asseraf

Deputy CEO

HarvestSimon Seiter

Managing Director and CFO / CPO

AllUnityDr. Til Rochow

CPO & Co-Founder

UpvestDr. Oliver Pfeil

Chairman of the Board

ÖKOWORLD AGJerome Evans

CEO

firstcoloAlexander Sperlich

Managing Director DE/ AT/ CH,

MorningstarDavid Niedzielski

Managing Director

Sprengnetter GroupSusanne Krehl

Chief Growth Officer

wealthAPIPablo Nobre dos Reis

Digital Products Analyst

DWSNicola Alvaro

Head of Wealth Services & Distribution

Allianz Life Luxembourg Ltd.

Leyla Kunimoto

Founder

Accredited Investor InsightsDr. Alexander Bechtel

Global Head of Digital Products

DWSDelphine Asseraf

Deputy CEO

HarvestSimon Seiter

Managing Director and CFO / CPO

AllUnityDr. Til Rochow

CPO & Co-Founder

UpvestDr. Oliver Pfeil

Chairman of the Board

ÖKOWORLD AGJerome Evans

CEO

firstcoloAlexander Sperlich

Managing Director DE/ AT/ CH,

MorningstarDavid Niedzielski

Managing Director

Sprengnetter GroupSusanne Krehl

Chief Growth Officer

wealthAPIPablo Nobre dos Reis

Digital Products Analyst

DWSNicola Alvaro

Head of Wealth Services & Distribution

Allianz Life Luxembourg Ltd.

Leyla Kunimoto

Founder

Accredited Investor InsightsDr. Alexander Bechtel

Global Head of Digital Products

DWSDelphine Asseraf

Deputy CEO

HarvestSimon Seiter

Managing Director and CFO / CPO

AllUnityDr. Til Rochow

CPO & Co-Founder

UpvestDr. Oliver Pfeil

Chairman of the Board

ÖKOWORLD AGJerome Evans

CEO

firstcoloAlexander Sperlich

Managing Director DE/ AT/ CH,

MorningstarDavid Niedzielski

Managing Director

Sprengnetter GroupSusanne Krehl

Chief Growth Officer

wealthAPIPablo Nobre dos Reis

Digital Products Analyst

DWSNicola Alvaro

Head of Wealth Services & Distribution

Allianz Life Luxembourg Ltd.

These are the WealthTech trends you should keep an eye on in 2026!

These are the WealthTech trends you should keep an eye on in 2026!

Resilience, AI, Cloud Sovereignty: The wealth management sector faces decisions in 2026 that cannot wait.

Which technologies will truly prevail? Where will measurable competitive advantages arise? And what regulatory changes will directly affect your business?

The WealthTech Radar 2026 provides the practical blueprint for this.

12 industry experts analyze the topics that will determine who leads the European wealth sector in the coming years.

Resilience, AI, Cloud Sovereignty: The wealth management sector faces decisions in 2026 that cannot wait.

Which technologies will truly prevail? Where will measurable competitive advantages arise? And what regulatory changes will directly affect your business?

The WealthTech Radar 2026 provides the practical blueprint for this.

12 industry experts analyze the topics that will determine who leads the European wealth sector in the coming years.

These are the WealthTech trends you should keep an eye on in 2026!

Resilience, AI, Cloud Sovereignty: The wealth management industry faces decisions in 2026 that cannot wait.

Which technologies will actually prevail? Where is measurable competitive advantage emerging? And what regulatory changes will directly affect your business?

The WealthTech Radar 2026 provides the practical blueprint for this.

12 industry experts analyze the topics that will determine who will lead the European wealth sector in the coming years.

Overview

WTR 2026

Delphine Asseraf, Harvest

81% of companies name AI as the most important technology of the decade. Only 25% use it as a genuine competitive advantage.

This chapter shows where the gap between aspiration and reality arises, and which levers banks and advisers can now set in motion concretely: from the RM copilot to automated suitability assessment, built on data foundations that will endure in the long term.

Delphine Asseraf, Harvest

81% of companies name AI as the most important technology of the decade. Only 25% use it as a genuine competitive advantage.

This chapter shows where the gap between aspiration and reality arises, and which levers banks and advisers can now set in motion concretely: from the RM copilot to automated suitability assessment, built on data foundations that will endure in the long term.

Dr. Alexander Bechtel & Pablo Nobre dos Reis, DWS

Stablecoins have reached a market capitalisation of US$300 billion. Bitcoin ETFs alone hold over US$145 billion in the US. MiCA is in force. The regulatory framework banks have been waiting for is here.

This chapter breaks down the three relevant crypto categories for wealth management and shows why integrating custody, access and advisory context into existing systems is no longer optional.

Dr. Alexander Bechtel & Pablo Nobre dos Reis, DWS

Stablecoins have reached a market capitalisation of US$300 billion. Bitcoin ETFs alone hold over US$145 billion in the US. MiCA is in force. The regulatory framework banks have been waiting for is here.

This chapter breaks down the three relevant crypto categories for wealth management and shows why integrating custody, access and advisory context into existing systems is no longer optional.

Dr. Oliver Pfeil, ÖKOWORLD AG

Two-thirds of German private investors are interested in sustainable investments. Only 14% actually invest in them. This is not a demand problem. It is a credibility problem.

This chapter examines the regulatory changes that will come into force from September 2026: what fund naming rules, SFDR obligations and the Empowering Consumers Directive mean in practice, and how advisers can turn ESG from a documentation burden into an advisory opportunity.

Dr. Oliver Pfeil, ÖKOWORLD AG

Two-thirds of German private investors are interested in sustainable investments. Only 14% actually invest in them. This is not a demand problem. It is a credibility problem.

This chapter examines the regulatory changes that will come into force from September 2026: what fund naming rules, SFDR obligations and the Empowering Consumers Directive mean in practice, and how advisers can turn ESG from a documentation burden into an advisory opportunity.

Nicola Alvaro, Allianz Life Luxembourg

64% of investors consider preparation for wealth transfer to be very important. Only 28% have been seriously addressed by their adviser about it. The great wealth transfer is already under way, and most institutions are still not part of the conversation.

This chapter explains what digital estate planning means across custodial accounts, private market investments, wallets and digital assets, and what banks must provide in order to remain relevant to both the transferring and receiving generation.

Nicola Alvaro, Allianz Life Luxembourg

64% of investors consider preparation for wealth transfer to be very important. Only 28% have been seriously addressed by their adviser about it. The great wealth transfer is already under way, and most institutions are still not part of the conversation.

This chapter explains what digital estate planning means across custodial accounts, private market investments, wallets and digital assets, and what banks must provide in order to remain relevant to both the transferring and receiving generation.

Leyla Kunimoto, Accredited Investor Insights

European private equity fundraising reached a new cycle high in 2024 at €140.9 billion. Digital platforms have simplified access and lowered minimum investments. For banks, the question is no longer whether private equity belongs in wealth portfolios, but how to integrate it without handing the client relationship over to fintech platforms.

This chapter shows the current state of private markets, how digital distribution is reshaping access for high-net-worth clients, and what a realistic integration path looks like for banks and advisers in the DACH region.

Leyla Kunimoto, Accredited Investor Insights

European private equity fundraising reached a new cycle high in 2024 at €140.9 billion. Digital platforms have simplified access and lowered minimum investments. For banks, the question is no longer whether private equity belongs in wealth portfolios, but how to integrate it without handing the client relationship over to fintech platforms.

This chapter shows the current state of private markets, how digital distribution is reshaping access for high-net-worth clients, and what a realistic integration path looks like for banks and advisers in the DACH region.

Jerome Evans, firstcolo

The AWS outage in October 2025 made visible what the industry has long known: cloud concentration is a systemic risk. At the same time, DORA obligations are taking effect, the US Cloud Act is creating ongoing data sovereignty conflicts, and the ECB has published new outsourcing guidelines.

This chapter examines what geopolitical tensions mean for cloud strategies in the financial sector, how DORA changes the outsourcing calculation, and which sovereign cloud alternatives are realistically available today for European banks.

Jerome Evans, firstcolo

The AWS outage in October 2025 made visible what the industry has long known: cloud concentration is a systemic risk. At the same time, DORA obligations are taking effect, the US Cloud Act is creating ongoing data sovereignty conflicts, and the ECB has published new outsourcing guidelines.

This chapter examines what geopolitical tensions mean for cloud strategies in the financial sector, how DORA changes the outsourcing calculation, and which sovereign cloud alternatives are realistically available today for European banks.

Simon Seiter, AllUnity

Tokenised money market funds, bonds and shares are already in use. Stablecoins are becoming settlement infrastructure. The market is moving from pilots into production, and the gap between institutions with ready infrastructure and those without is widening quickly.

This chapter covers the three tokenisation layers that will be decisive in 2026, where real traction is emerging and where the hype still outweighs reality, and how banks can position themselves on the right side of the new settlement infrastructure.

Simon Seiter, AllUnity

Tokenised money market funds, bonds and shares are already in use. Stablecoins are becoming settlement infrastructure. The market is moving from pilots into production, and the gap between institutions with ready infrastructure and those without is widening quickly.

This chapter covers the three tokenisation layers that will be decisive in 2026, where real traction is emerging and where the hype still outweighs reality, and how banks can position themselves on the right side of the new settlement infrastructure.

Alexander Sperlich, Morningstar

Direct Indexing has been an institutional tool for decades. Lower minimums, better technology and growing demand for customisation are now bringing it into broader Wealth Management. For advisers, it is one of the few ways to deliver measurable, individual added value that a standard fund cannot replicate.

This chapter explains how Direct Indexing works in practice, where it generates the greatest tangible client benefits (tax efficiency, ESG alignment, factor tilts), and what infrastructure wealth managers need to offer it without additional operational complexity.

Alexander Sperlich, Morningstar

Direct Indexing has been an institutional tool for decades. Lower minimums, better technology and growing demand for customisation are now bringing it into broader Wealth Management. For advisers, it is one of the few ways to deliver measurable, individual added value that a standard fund cannot replicate.

This chapter explains how Direct Indexing works in practice, where it generates the greatest tangible client benefits (tax efficiency, ESG alignment, factor tilts), and what infrastructure wealth managers need to offer it without additional operational complexity.

David Niedzielski, Sprengnetter

Property is the largest asset class held by most private clients, and at the same time the least integrated in the wealth management advisory process. Valuations are outdated, data is fragmented, and advisers often have no reliable picture of what a client actually owns.

This chapter shows how digital valuation data and platform integration can change that, what role property plays in a holistic view of wealth, and how banks and advisers can incorporate property into portfolio advice without having to become property specialists.

David Niedzielski, Sprengnetter

Property is the largest asset class held by most private clients, and at the same time the least integrated in the wealth management advisory process. Valuations are outdated, data is fragmented, and advisers often have no reliable picture of what a client actually owns.

This chapter shows how digital valuation data and platform integration can change that, what role property plays in a holistic view of wealth, and how banks and advisers can incorporate property into portfolio advice without having to become property specialists.

Dr. Til Rochow, Upvest

Most wealth management platforms run on infrastructure that was not built for today’s products, speeds and customer expectations. The backend is where digital transformation either becomes reality or stalls.

This chapter describes what a modern, API-based wealth backend looks like, which components banks should build themselves and which they should buy, and how modular infrastructure enables the product flexibility and speed to market that legacy core systems block.

Dr. Til Rochow, Upvest

Most wealth management platforms run on infrastructure that was not built for today’s products, speeds and customer expectations. The backend is where digital transformation either becomes reality or stalls.

This chapter describes what a modern, API-based wealth backend looks like, which components banks should build themselves and which they should buy, and how modular infrastructure enables the product flexibility and speed to market that legacy core systems block.

Susanne Krehl, wealthAPI

Most clients hold assets with several custodians, banks and platforms. Most advisers still piece this picture together manually. Without a consolidated view, personalised advice at scale is not possible.

This chapter explains how Wealth Aggregation works today, what Open Banking and access to account data mean for the quality of advice, and how banks and independent advisers build the holistic client view that is increasingly a basic expectation, not a differentiator.

Susanne Krehl, wealthAPI

Most clients hold assets with several custodians, banks and platforms. Most advisers still piece this picture together manually. Without a consolidated view, personalised advice at scale is not possible.

This chapter explains how Wealth Aggregation works today, what Open Banking and access to account data mean for the quality of advice, and how banks and independent advisers build the holistic client view that is increasingly a basic expectation, not a differentiator.

Sneak preview

Sneak preview

A first look at selected trends. The complete WealthTech Radar 2026 is available for free as a PDF.

A first look at selected trends. The complete WealthTech Radar 2026 is available for free as a PDF.

The blueprint for Europe's wealth management industry

The blueprint for Europe’s wealth management industry

The blueprint for Europe's wealth management sector

Download WealthTech Radar 2026 now for free!

Download WealthTech Radar 2026 now for free!

Download WealthTech Radar 2026 now for free!

Fincite GmbH

Franklinstr. 52

60486 Frankfurt

Wealth management/

Financial planning

Modular wealth

management software

Features fincite • cios

Follow us on:

Fincite GmbH

Franklinstr. 52

60486 Frankfurt

Wealth management/

Financial planning

Modular wealth

management software

Features fincite • cios

Follow us on:

Fincite GmbH

Franklinstr. 52

60486 Frankfurt

Wealth management/

Financial planning

Modular wealth

management software

Features fincite • cios

© 2026 Fincite GmbH. All rights reserved.

Follow us on: